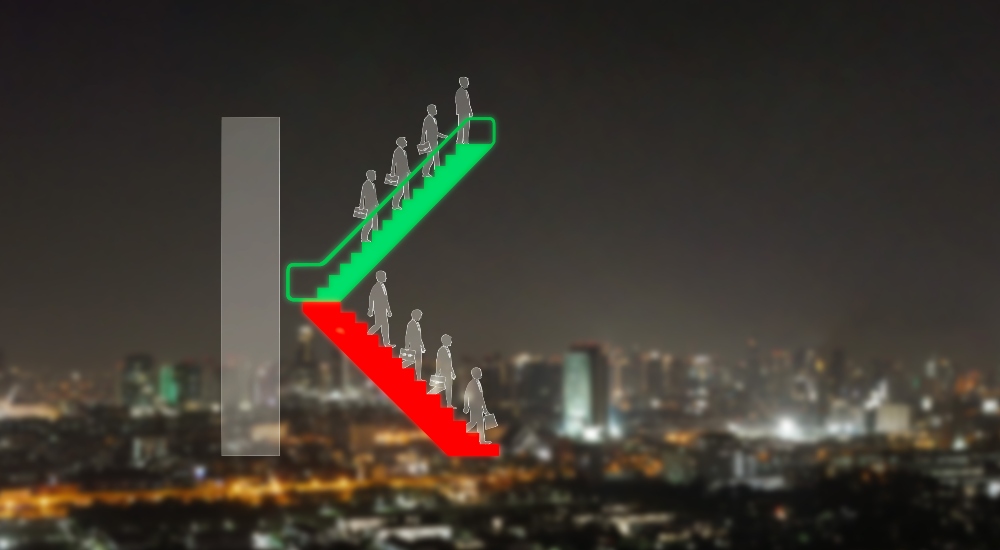

Takeaways

- K-Shaped economy forming in CI where outsized performance of certain firms is masking larger than average losses.

- One in five firms on D-Tools saw over 21% decrease in sales.

- Contracts now draw almost 3/4 of their value from equipment due to rising costs.

The D-Tools Year in Review Report for 2025 has unveiled a potential bifurcation within custom integration (CI) that may be developing into its own K-shaped economy.

While the industry seemed to grow its sales by 18.8% on average, that rate masks a severe distribution skew. The reality is that beneath that average, a sizeable portion of the industry saw staggering losses, masked only by the outsized gains seen at the opposite end.

What’s strange, however, is that the difference in performance isn’t necessarily tied to a firm’s annual revenue or clientele, with the real cause for the split still undetermined.

D-Tools Year in Review Highlights K-Shaped Economy Developing in CI

The start of 2025 proved to be rocky for many firms, as questions regarding tariffs and other elements of economic uncertainty throttled business in the beginning. While the latter half of the year provided relief for some, D-Tools’ Year in Review is helping to paint a picture of how skewed that recovery seems to have been.

The average paints a picture of 18.8% sale growth across all firms; however, that growth is split between massive losses and meteoric gains at both ends of the industry. While 35% of firms posted gains of 51% or more, 20% reported losses of over 21%.

This revelation correlates somewhat with CE Pro’s own findings in its 2026 State of the Industry, where a large portion of firms expected revenues to remain flat in 2026. The revelation D-Tools provides is the scope at which more successful firms seem to be propping up industry growth.

What’s curious, however, is that, according to D-Tools, these gains and losses are not strictly correlated with sales size overall. Companies making in excess of $5 million in sales are still seeing massive drops from prior years, just as smaller firms are seeing substantial growth.

The Effects of Tariffs Rear Their Head

On the topic of tariffs, the effects of last year’s policies seem to also be finally appearing within the balance sheets of businesses. While sales rates (on average) grew in 2025, the national average gross margin shrank, moving from 41% in 2024 to 38.6% in 2025, all this while the average contract value rose 5.2%, nearly double the national rate of inflation.

Digging deeper into the splits of those contracts, the source of inflation becomes clear. 76% of the contract value in 2025 was attributed to equipment compared to 24% from labor. This mirrors the findings in CE Pro’s 2026 Wage and Salary Study that found that, apart from sales representatives, pay remained largely unchanged from 2023.

That shrinking margin was also the most pronounced in the South, where, despite having the cheapest labor rates of the nation, a slowing housing market and rising equipment costs seems to be eating more into the revenues of firms within the region.

When it Comes to Proposal Success, Speed is King

One curiosity uncovered when trying to assess what might contribute to a successful sale is how much speed plays a role in a successful proposal. While the national average close rate sits at 69.7%, firms that can deliver a proposal in 48 hours see a staggering 88% win rate. The slowest quartile (60+ days to deliver a proposal), in contrast, sits at 69.6%.

But does project complexity play a role? While the specifics between those 48 hour proposals aren’t given, less complex projects are able to close faster, given that these projects require only one proposal, generally. Larger projects in contrast, average between eight or nine proposals. Regardless, speed remains king across all levels of complexity.

In Summary

While the information here encapsulates only a small amount of the data found in D-Tools’ report, the story it depicts is striking for the industry. While industry growth remains steady, a growing divide is being highlighted between firms, mirroring the K-shaped economy in the U.S. Massive outperformers are covering the losses occurring at other ends of the industry. The only difference is larger, more historically profitable firms are just as susceptible to these outsized losses as smaller firms are to larger than average gains.

At the same time, tariffs and supply chain issues seem to be accelerating equipment costs, eating into margins. This is even more striking when you consider the $1+ million revenue marker that serves as a very real barrier of growth for firms at times. While larger firms can more readily shoulder these extra expenses up front, smaller firms cannot, and where growth stalls, these costs may be catching up. The fact that outsized gains and losses appear to be occurring at all strata, however, does warrant more information before a thorough conclusion can be drawn.

For readers that want to dig into it themselves, a full download of D-Tools Year-in-Review for 2025 can be accessed for free on the D-Tools website.