According to CE Pro‘s sister publication Security Sales & Integration and its recent collaborative survey with Parks Associates, about half of nearly 200 surveyed residential security dealer respondents anticipate revenue growth of at least 10% in 2019 as compared to the prior year.

The latest study offers evidence of a continuing strong market, but also ongoing industry challenges. Given margin of error, the expectations noted above parallel the revenue growth percentage dealers reported for 2018 over 2017.

While percentages of security dealers expecting growth are lower in both years than the larger percentages seen in 2013-2016, 50% still indicates a continued strong marketplace. Those earlier high growth percentages occurred as the United States emerged from the Great Recession. As important, a scant 5% report lower revenues expected in 2019.

This market stability continues even while new starts and home resales have been quite flat in the past two years.

Impact of DIY

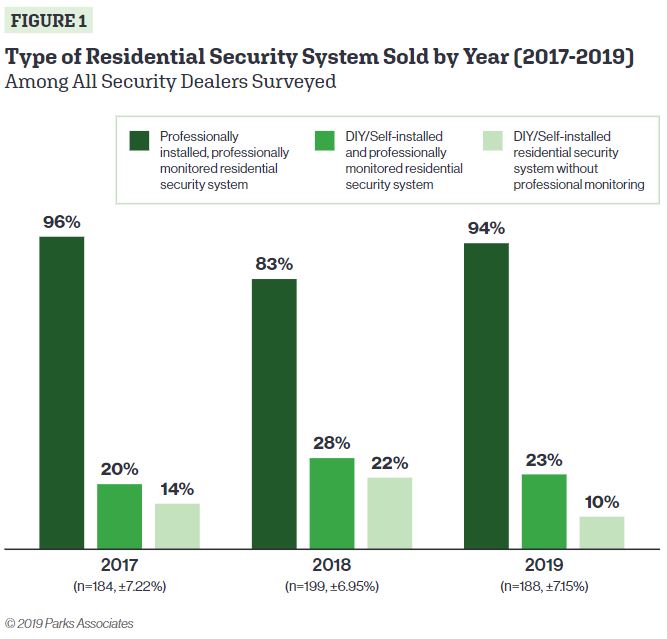

In 2019, sales of DIY systems decreased from 2018 (Figure 1). While some of that decline may result from margin of error given sample sizes, it may also foreshadow that DIY offerings have lost some of their appeal. Only 24% of responding dealers report selling DIY systems, which is flat from 2018.

The percentage of dealers selling DIY systems without professional monitoring dropped more than 50% between 2018 and 2019 (Figure 2). Nonetheless, there remains solid interest in adopting and offering DIY systems among dealers not doing so now. Among the 75% of security dealers that do not offer DIY systems, 27% (about 20% of all dealers) report a high intention to add them in the next year.

The main reason, offered by half of these dealers, is that their customers are asking about DIY devices. If a dealer has little or no enthusiasm for the products, it will not highlight their benefits any more than necessary to prospects.

This points to the power of consumer demand. After running these numbers through forecasting methodology, Parks Associates forecasts that 5%-7% of dealers will adopt DIY systems in the next year. Another question remains: how many dealers currently selling DIY systems will abandon those efforts?

The sales split for the 25% of security dealers currently selling DIY systems as well as professionally installed systems is the same in 2019 as it was in 2018 (Figure 3).

Smart Devices & Support Demand

An increasing percentage of dealers sell security systems that include smart home products (Figure 4). In the 2018 dealer survey, 30% reported selling systems with smart home devices while 35% sold basic interactive systems. This year shows a nearly 50% increase in system sales with smart home devices.

As anticipated, dealers are migrating to include more smart home and networked video devices as they become comfortable with product features and reliability. Their customers are also more familiar with these devices than in the past, making it easier for dealers to explain benefits. Smart home devices often provide more stickiness for their dealers; they also provide more revenue.

Virtually all of the responding dealers offer smart home devices, but most of their system sales only include one or two devices, if any at all. Sales of smart home devices are up year over year or have close to parity with 2018 except networked security cameras (Figure 5).

The percentage of systems sold with cameras dropped in 2019 from 2018. Parks Associates and SSI will watch this closely to determine if this is an anomaly or if concerns over privacy and security dampen these sales. Even with that drop, network security cameras are the top selling smart home product with video doorbells and smart smoke detectors earning a close second and third place.

Parks Associates’ quarterly 10K consumer surveys show households value video cameras as a source of security, but do indeed have some concern for privacy. Retail is also the leading channel for smart home devices and may be cutting into the dealer channel. Dealers must face consumer concerns upfront, reassuring them as possible that their smart home devices are secure.

Accompanying the increase in smart home device sales is an increase in customer support needs. Householders acquiring these devices are not “techies” and challenges in usage or reliability frustrate them greatly.

Security dealers recognize this, with the highest percentage of dealers citing “ease of consumer use” as a No. 1 or 2 priority factor when they determine which brands and product types to adopt and offer their customers.

When consumer ease of use has the second highest percentage of dealers ranking it as a top priority, the first is ease of installation for the dealer. Those two factors go back and forth as the most important from a list of 14 choices. Notably, price falls below ease of use and install in ranking.

More than four in 10 respondents (42%) find that supporting smart home devices is very impactful to their businesses; support is costly for dealers (Figure 6). More than 60% report that the impact is high or very high. All but “value” security system dealers are migrating to smart home device selling.

Manufacturers with the most reliable and easy-to-use devices deserve whatever wins they earn. A little more than two in 10 security dealers (22%) report that a truck roll is the most often used solution to resolve a customer’s smart home issue, while 40% report that they most often resolve issues via a phone call. Truck rolls are expensive; it only takes a few to wipe out potential profit from a customer for the year.

Pricing Pressures

Average end-user prices for security systems with smart home devices declined nearly 20% in 2019 over 2018 (Figure 7). Several reasons can cause this. First, there may be fewer smart home devices selling per system even as more security system sales include at least one smart home device. In addition, the price of devices has declined and there are more brand options.

For example, Honeywell’s (Resideo) smart thermostat costs significantly less than a Nest smart thermostat. Also, installation of smart home devices may be easier than in the past or it may simply be that the learning curve has helped dealers become more efficient in installation.

Finally, Parks Associates’ interviews with security dealers indicate they value the added stickiness that selling smart home devices provides to their professional monitoring service. Some dealers may discount initial prices to obtain that stickiness as well as to earn higher monitoring fees.

RESULTS: Click here for the full results of the survey

Average aggregated professional monitoring fees across all customers for all types of monitoring are $44 for 2019, up from $42 in 2018. There are different monthly fee rates for various types of professional monitoring. Basic monitoring is at a low $39 dollars per month but that represents a year-over-year increase of nearly 20%.

All other monthly rates are quite flat with the exception of professional monitoring with basic interactive and smart home device services. That rate has a decline of 10% year over year. Parks Associates has predicted and predicts competitive pressure on monitoring fees; that is happening now. Still, fees are higher by 15%-20% for dealers selling smart home devices with their core security systems; that increase, added to increased stickiness, appeals to most dealers (Figure 8).

Moreover, and unsurprisingly, dealers report higher monthly fees for new customers than on average. Professional monitoring-only fees for customers signing up in 2019 are reported as $53 per month on average, while fees for professional monitoring with interactivity and video storage are $69 on average in 2019. All but “value” security dealers want these added dollars.

Top Challenges Ahead

While the residential security marketplace is stable today, there remain challenges and consolidation activity (Figure 9). And, of course, change. Interlogix, for example, just announced it is winding down its security control panel business in order to focus on other more lucrative areas.

Dealers report a whopping 25% (mean) attrition rate; that is so high that Parks Associates questions whether some dealers define attrition differently than the overall industry. Regardless, attrition eats into progress whether it is 14% or 20%. Labor markets are tight all over the nation; this may be particularly difficult for security companies that need installers who also understand networking technology.

Somewhat surprisingly, false alarms rank as the No. 2 challenge — still. Activations of self-installed DIY and self-monitored devices and systems may be causing increased concerns there; that remains to shake out.

Parks Associates forecasts a flat to slow growth market for the near future (Figure 10). The percentages are for all households with a functioning security system. Rates of adoption for 2019 over 2018 do not register a full 1%.

While growth is slow, householders who acquired their security system in 2019 have higher rates of adoption for smart home devices. For example, overall 11% of security households have a smart thermostat, but 19% of customers who acquired a security system in 2019 acquired a smart thermostat at the same time.

Tricia Parks is CEO and Dina Abdelrazik Senior Analyst for Parks Associates.